-

0000000

Transactions

-

0000000

Merchants

-

0000000

Countries

-

0000000

Deals

Buy and Sell Digital Assets

Over 1,091,812 members are onboard, so what are you waiting for?

Why choose TechBank?

We have what you need

our apps

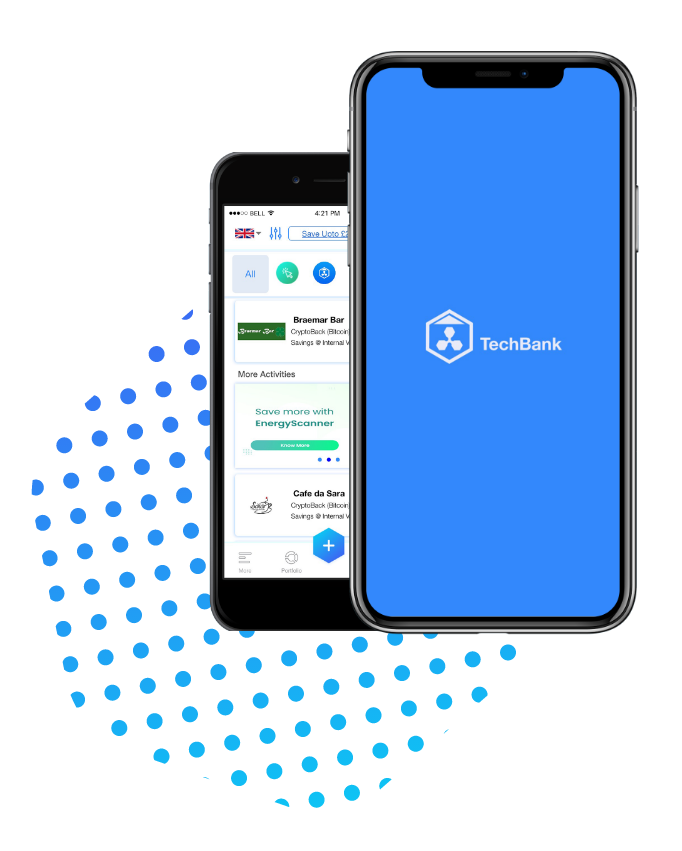

CeFiTechBank

CeFiTechBank

No Cards - No Fiat - No Fees.

Buy, Sell and manage your crypto over 60 popular Currencies in one place. We have built a fully functional and secure platform to manage your crypto portfolio. Our live App directly connects customers with local and international brands by allowing users to spend crypto with ease using our cutting-edge technology. The retailer API connected with the App issues instant e-codes, which can be scanned at checkout or redeemed online globally at major brands.

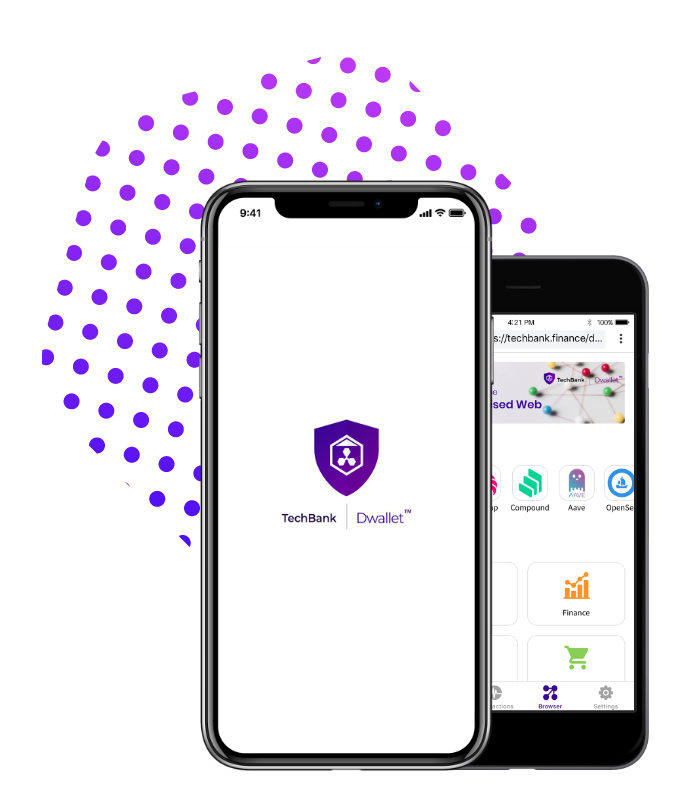

DeFiTechbank DwalletTM

DeFiTechBank DwalletTM

Whether you are an experienced user or brand new to blockchain, TechBank Dwallet helps you connect to the decentralized web: a new internet.

We're trusted by millions of people across the world, and our mission is to make this new decentralized web accessible to all.

our team

{{member.name}}

{{member.design}}

our team regulary speaks at and attends industry events

Get in touch

Drop in a message and we will get back to you as soon as we can.

Fill All Required Fields

Thanks For Contacting Us , We Will Get Back you soon